Relay Therapeutics: Updates, Progress, and an Evolving Buyout Narrative

As Phase 3 advances and valuation rises, the window for a takeover may be closing faster than expected.

If we set aside all the complex and frankly depressing developments around the war in Iran, along with their obvious impact on equity markets, I didn’t see much in terms of meaningful stock reactions driven by new fundamentals. If anything, price action seemed to hinge almost entirely on what Trump did or didn’t say.

The outlier keeping my portfolio afloat

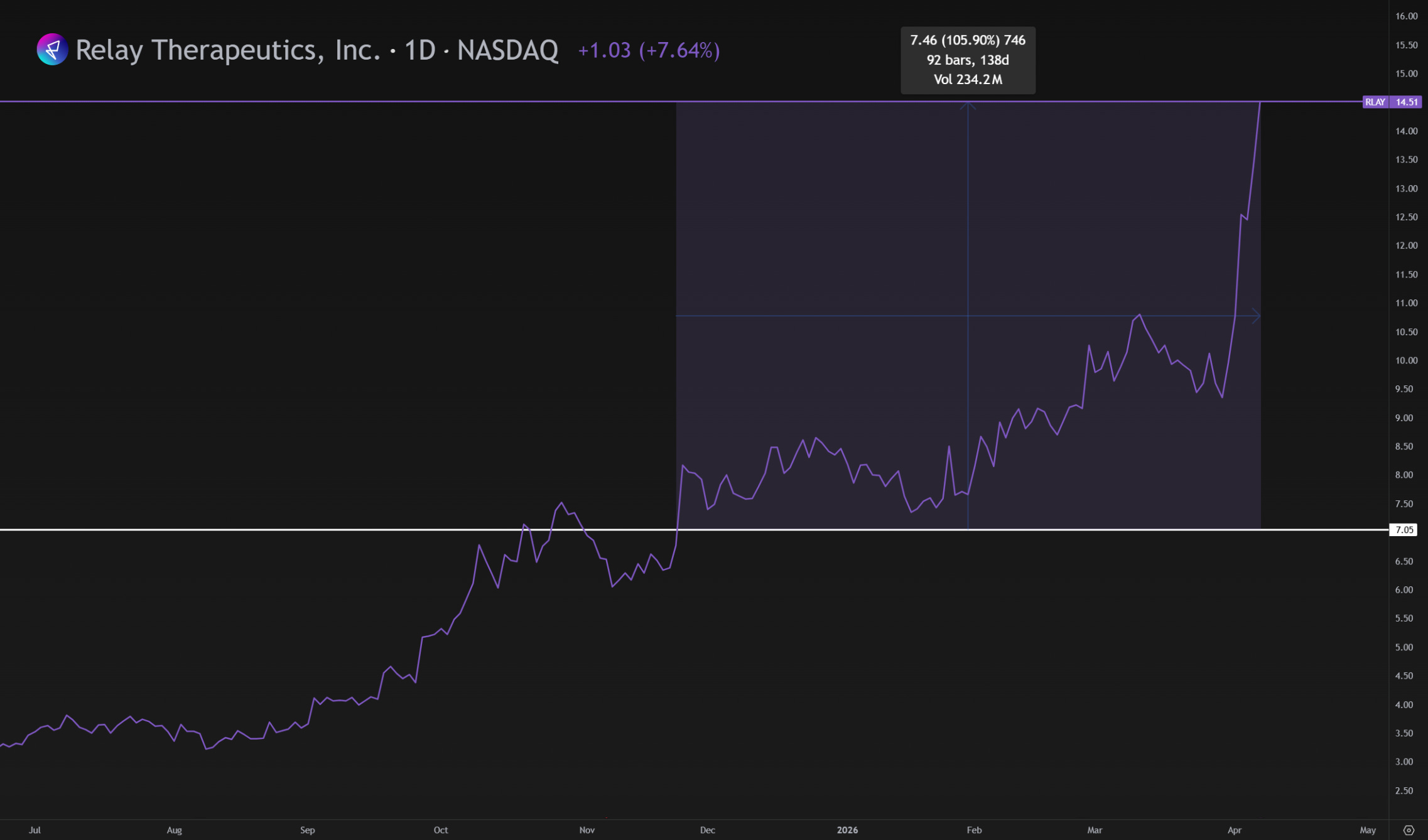

While the indices have pulled back 7-12% from their ATHs, dragging most of my positions down with them, there has been one exception: Relay Therapeutics.

As I’ve mentioned a few times before, I don’t usually invest in biotech stocks. However, back in early November 2025, I stumbled upon Relay and spent several weeks doing a deep dive into the company.

I really got pulled into it, and after some time, I managed to piece together the broader context around PI3Kα inhibitors and their current standard-of-care position in oncology, specifically in treating patients with HR+/HER2− (hormone receptor-positive, HER2-negative) advanced or metastatic breast cancer.

Relay Therapeutics: Pfizer’s Missing Puzzle Piece?

I have to admit, investing in biopharmaceutical companies has never really appealed to me. It is difficult to do a classic, solid analysis based on quarterly results, nor can one objectively assess the quality of the product or service, as we often have no idea if the research will ever reach a successful conclusion. It feels a bit like walking into a b…

Relay intrigued me so much that it actually became the first topic I ever wrote about here on my Substack. I went through clinical trial databases, looked into the institutions currently running those trials, discovered that Google Ventures had taken a stake, reviewed the study data and outcomes, and at the same time tried to assess toxicity risk, and therefore the probability of clinical failure.

At some point, I came to the conclusion that their drug, RLY-2608, is ambitious enough that the likelihood of failure is, in my view, unusually low.

I built this into one of my top three main positions, buying in three stages at an average cost basis of $7.05. With the stock now trading at $14.50, I’ve just hit a major milestone with over 100%+ return in around 140 days.

Disclaimer: I cannot guarantee the accuracy or timeliness of the information provided herein. This article does not constitute financial advice, an investment recommendation, or a factual basis for your investment decisions. Please conduct your own due diligence.

A few recent updates

On December 12, 2025, at the San Antonio Breast Cancer Symposium (SABCS), Relay delivered a presentation. While digging through their ePoster, I noticed several key pieces of information.

The transition from RLY-2608 to Zovegalisib

This was a quiet change, at the time, it hadn’t been formally announced anywhere, and the only place you could catch it was in these newly released materials exclusive to SABCS. The use of the International Nonproprietary Name (INN) right in the headline of one of the year’s key conferences was, to me, a strong signal that the drug is transitioning from the lab phase into commercialization and brand-building.

In other words, the company is signaling that it considers the molecule essentially market-ready.

Dr. Hope S. Rugo

Another notable detail was the addition of a new author on the Re-Discover 2 study: Dr. Hope S. Rugo. She’s a globally recognized authority in breast oncology from UCSF, and her role as lead author acts as a strong signal of credibility and confidence in the drug’s potential. Experts of this caliber typically don’t attach their names to projects that lack a clear path forward.

At the same time, the ePoster confirmed that Phase 3 is progressing as planned, with recruitment ongoing.

I won't be sharing the ePoster here, as it was part of a paywalled section for conference attendees, but it’s worth noting that Relay eventually released all the relevant data from this document in their own public materials later on.

Eli Lilly and their LY4064809 (STX-478)

Relay wasn’t the only one presenting at SABCS, competition showed up as well.

Despite Eli Lilly spending $2.5 billion to acquire the program from Scorpion Therapeutics, the data presented in their ePoster pointed to safety issues that Relay simply doesn’t have.

In monotherapy, LY4064809 showed a 14% rate of severe liver enzyme elevation (Grade ≥3). In oncology, liver toxicity is a deal-breaker, it limits the ability to safely combine the drug with other therapies that are also metabolized in the liver.

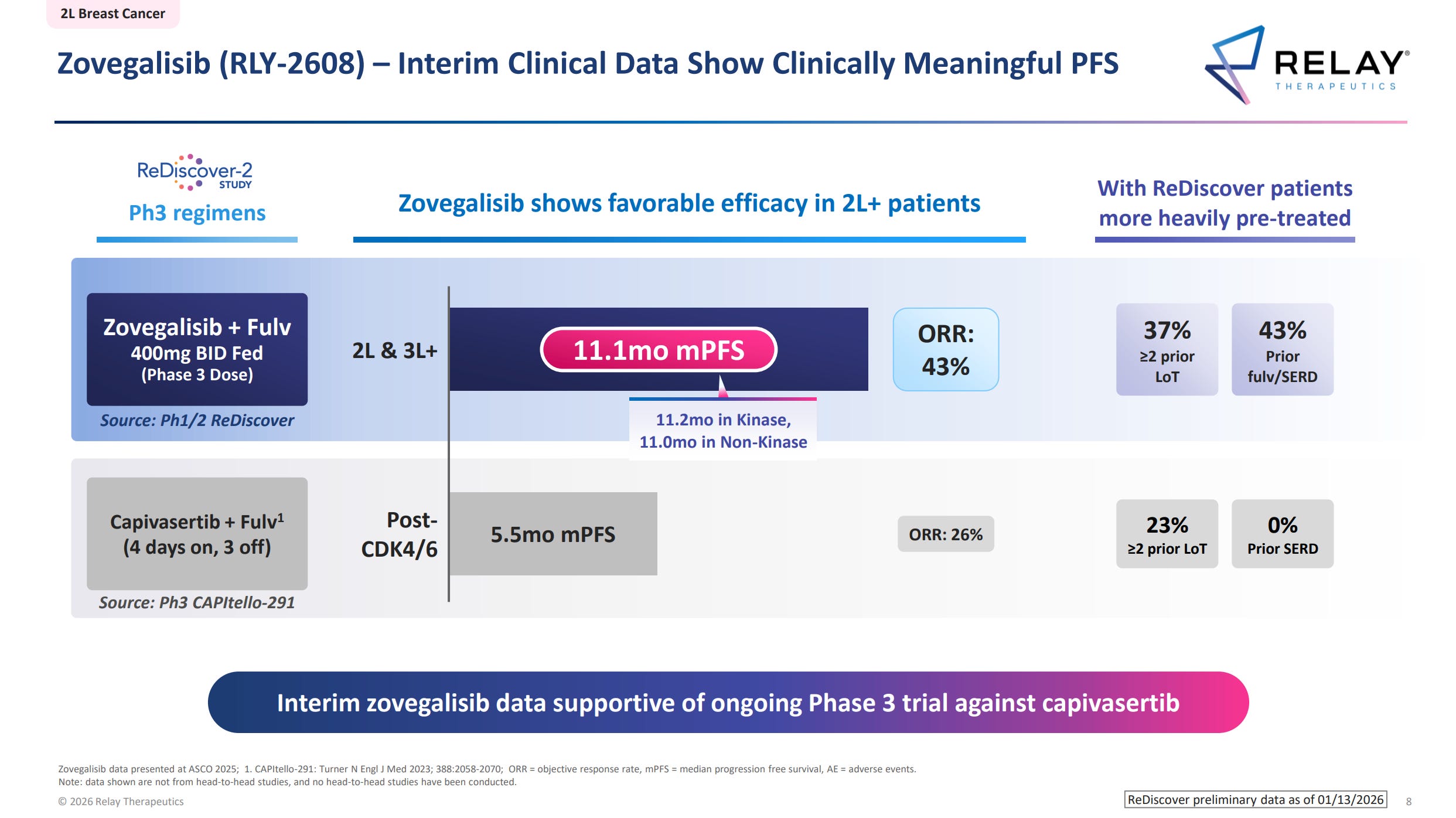

By comparison, Zovegalisib from Relay Therapeutics demonstrates a clean liver profile, which gives it a major strategic advantage for future combination regimens.

Then there’s the issue of general tolerability and metabolic burden. The competitor’s drug is proving to be too toxic at effective doses. Nearly a third of patients (28%) had to reduce their dosage due to side effects, suggesting that Eli Lilly has missed the ideal therapeutic window.

What’s also telling is their rush into Phase 3. A deep dive into the PIKALO-2 study design reveals a company acting under pressure. While they’ve officially labeled it a Phase 3 trial, they’ve included a dose optimization lead-in.

In practice, that means they are still trying to determine a safe dose at this late stage and don’t yet have a fully locked protocol. While Relay is already recruiting for Phase 3 with a clear, safe, and established dose of 400 mg, Eli Lilly is still working through toxicity issues on the fly, significantly increasing the risk of trial failure.

Even though Eli Lilly’s drug is biologically active and capable of reducing circulating tumor DNA (ctDNA), its safety profile is messy. The combination of elevated liver risk, frequent dose reductions, and hematological issues (such as neutropenia in combination settings) makes it a poor candidate for clean triple-combination regimens, something companies like Pfizer are actively pursuing.

My own Q&A with Relay

During SABCS, I signed up for virtual access to follow the conference from home. While watching, I noticed the moderator was actively picking questions from the virtual Q&A window. I didn’t hesitate and submitted a question of my own, a subtle attempt to sniff out any potential M&A interest.

My question: “RLY-2608: In ReDiscover triplets, does the safety profile suggest an optimal CDK4/6 partner for the frontline strategy?”

The question targeted the drug’s strategic future in the frontline setting (first-line treatment). My core thesis is that thanks to its exceptionally clean toxicological profile, specifically the lack of hepatotoxicity and hyperglycemia, Zovegalisib is the perfect candidate for triple combinations with CDK4/6 inhibitors.

I wanted to see if the safety data already favored a specific partner: Pfizer (Atirmociclib, Palbociclib) or Novartis (Ribociclib). Identifying a favorite would directly point to who the most likely suitor for Relay Therapeutics might be.

The answer was, unsurprisingly, quite neutral:

“Thank you for the question. In the first-in-human trial, all the cohorts are testing different triplets, but these combinations are on very early days and the toxicity profile hasn’t been reported yet.” — Cristina Saura, MD, PhD

Diplomatic answer, however, for me, it was actually good news. By stating they are testing various combinations without naming a favorite, Relay is keeping all doors open. The phrase that toxicity profile hasn’t been reported yet doesn’t mean they don’t have the data, it just means they aren’t going public with it yet. If there were any significant safety issues, I believe we would have seen red flags by now.

Granted Breakthrough Therapy Designation by U.S. FDA

Another major update arrived on February 3, 2026. Relay announced that the FDA has granted Breakthrough Therapy Designation (BTD) to Zovegalisib (RLY-2608), in combination with fulvestrant for the treatment of PIK3CA-mutated HR+/HER2- advanced or metastatic breast cancer.

This decision is based on the strong data generated so far from the ReDiscover Phase 1/2 study and signals that the FDA sees the therapy as potentially meaningfully superior to the current standard of care.

BTD status also enables a more accelerated development pathway, closer interaction with the regulator, and potentially a shorter route to approval.

In my view, this BTD is a massive green flag for shareholders. Most importantly, it significantly de-risks the clinical and regulatory thesis, as the FDA is indirectly validating the quality and impact of the data seen so far. This designation makes Relay an even more attractive player in the space, and I expect this quality stamp to eventually be reflected in the company’s valuation.

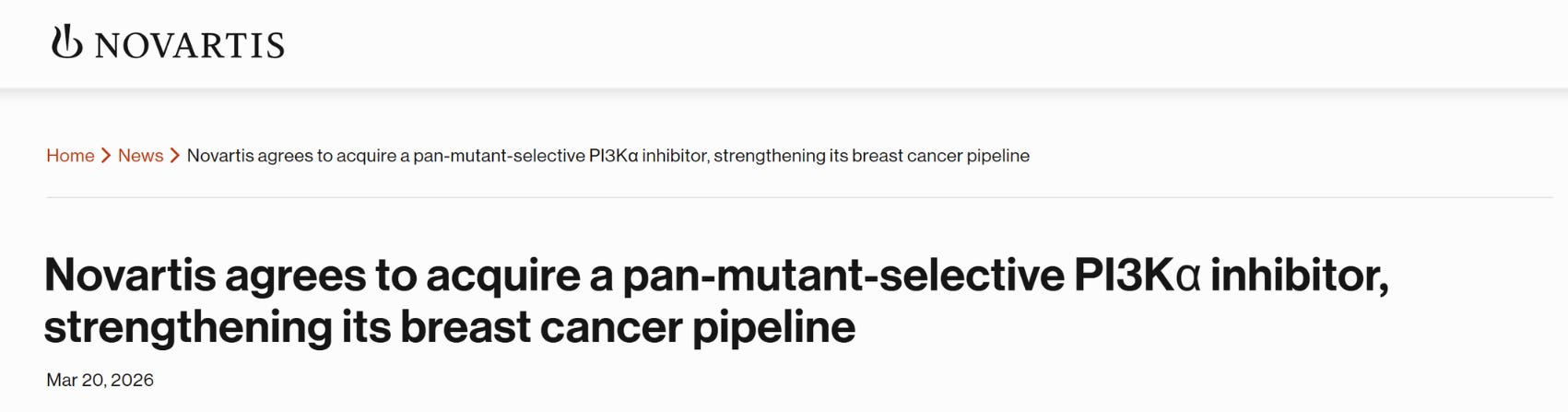

Novartis Acquires SNV4818

As it turns out, I wasn't far off. Novartis was indeed scouting for a successor to its current treatment portfolio, and on March 20, 2026, the deal became official.

Novartis agreed to acquire Synnovation Therapeutics’ subsidiary, Pikavation Therapeutics, in a deal worth up to $3 billion ($2B upfront, $1B in milestones). The deal centers on acquiring SNV4818, a pan-mutant-selective PI3Kα inhibitor designed to treat HR+/HER2- breast cancer with fewer side effects.

This effectively removes Novartis from our original M&A equation, leaving Pfizer as the primary remaining suitor. Or maybe not. More on that later.

And it actually makes sense.

Until recently, SNV4818 had been flying relatively under the radar compared to Zovegalisib. The company operated more quietly, and the drug only recently entered Phase 1 clinical trials. From that perspective, Novartis’ move fits the classic big pharma playbook.

The key factor here was likely a buy vs. build decision.

While Relay Therapeutics has a more advanced program already in Phase 3, acquiring the company outright would likely cost somewhere in the $5–10 billion range. In contrast, SNV4818 was secured at a significantly lower price, while allowing Novartis to retain full control over development and intellectual property. That translates into greater flexibility and potentially higher long-term upside without the need for complex partnerships.

Footnote: Relay is already in Phase 3, yet its market cap still sits below $3B.

This deal only reinforces how strong the demand for PI3Kα inhibitors currently is. And it may very well explain the recent sharp move in the stock price of Relay, which did +47% over the past month alone.

M&A: Pfizer or AstraZeneca?

I was previously convinced that Pfizer was the prime candidate to acquire Relay. As I mentioned, we have confirmation that they are currently testing the efficacy of Atirmociclib in triplet combinations with RLY-2608 and Fulvestrant.

This testing is further backed by data-sharing agreements. If Pfizer truly wants to replace Ibrance (Palbociclib) as it approaches its patent cliff, and if they hope to compete with Roche’s Inavolisib, they have no choice but to aggressively pursue these triple combinations.

That said, I’m no longer entirely convinced that Pfizer is in the right position to pursue new acquisitions at the moment.

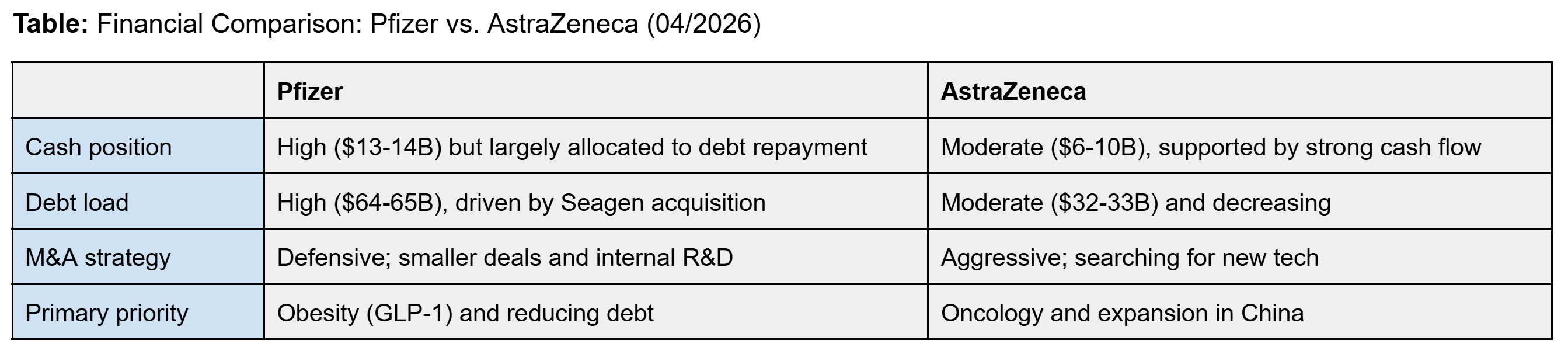

The financial positioning of these pharma giants has diverged quite significantly in 2026, and their strategic priorities reflect that.

While Pfizer is currently in a consolidation phase following expensive acquisitions and declining post-pandemic revenues, AstraZeneca continues to execute on an aggressive growth strategy, targeting $80 billion in annual revenue by 2030.

This shift in the landscape changes everything

While Pfizer has substantial financial resources, it is currently prioritizing capital discipline. Following the $43 billion acquisition of Seagen, or the more recent Metsera and the decline in COVID-related revenues, the company is primarily focused on deleveraging and investing in new growth areas, most notably obesity (GLP-1), where it is advancing a large-scale clinical program.

In oncology, Pfizer already holds a strong internal asset in its CDK4 inhibitor Atirmociclib, making it a natural partner for combination strategies with Zovegalisib.

It’s entirely possible that such a partnership could be sufficient from Pfizer’s perspective. Structuring the relationship as a partnership rather than an acquisition would also minimize capital intensity.

AstraZeneca, on the other hand, is positioning itself as a far more aggressive player. Oncology is their lifeblood, accounting for roughly 45% of their total revenue. While their current AKT inhibitor, Capivasertib, has shown efficacy, the AKT class is notorious for hitting a ceiling due to toxicity issues. It is also not as efficient.

If Zovegalisib’s clinical data (specifically from ReDiscover-2) proves to be superior, acquiring Relay wouldn’t be just a portfolio expansion for AstraZeneca, it would be a defensive move to protect its dominant position in breast cancer treatment.

The Novartis acquisition of the SNV4818 program in March 2026 sent a loud signal regarding the value of the selective PI3Kα market. For Pfizer, it’s a warning, they risk losing their strategic edge in combination therapies if Relay is snatched up by a competitor. For AstraZeneca, it’s a clear indicator that the competition is already building alternatives. Staying on the sidelines without a proprietary selective inhibitor could mean a permanent loss of competitiveness.

From this new perspective, AstraZeneca appears to be the more likely acquirer.

It has stronger strategic motivation and fewer constraints when it comes to capital allocation. Pfizer, while offering clear synergies, is currently more likely to take a cautious approach given its financial priorities.

Vascular malformations and NRAS

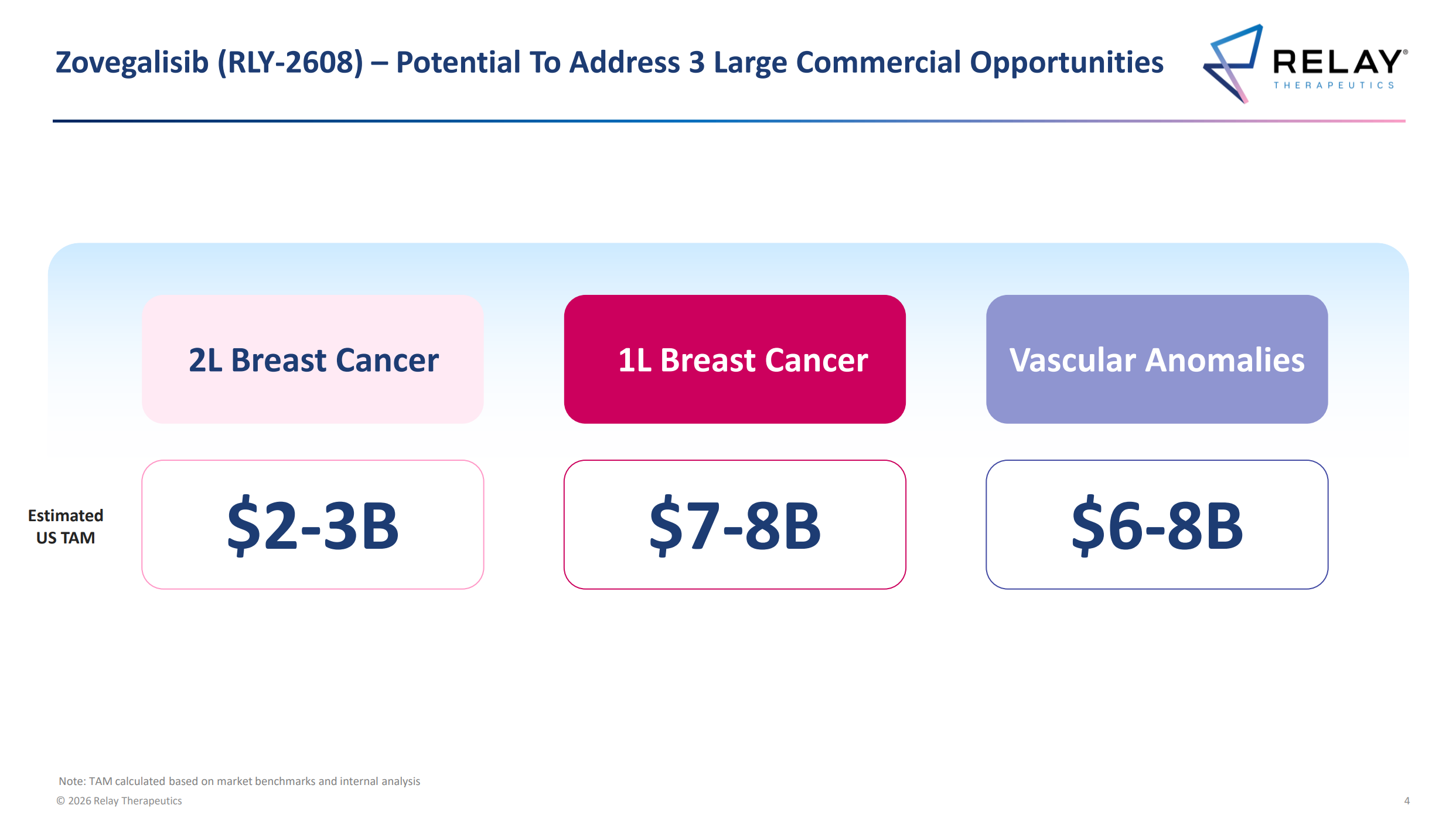

As of April 2026, Zovegalisib is estimated to have a cumulative U.S. market potential of approximately $15–19 billion. The largest share comes from the frontline breast cancer setting ($7–8 billion), followed by second-line treatment ($2–3 billion), and the vascular anomalies segment ($6–8 billion).

The vascular anomalies segment, in particular, is emerging as a major growth engine. Relay estimates that these conditions affect up to 170,000 patients annually in the U.S. Currently, there is no approved selective treatment available, and existing treatments show relatively low efficacy (around 11–27%), which suggests Relay could potentially capture a dominant share of this market.

The RLY-8161 program, targeting NRAS mutations, represents another, somewhat under-the-radar, but highly significant opportunity within the company’s pipeline. These mutations occur in roughly 29,000 new patients per year in the U.S. and are associated with aggressive cancers, including melanoma, colorectal cancer, and thyroid cancer.

Just as with PI3Kα, there is currently no approved selective NRAS inhibitor on the market, positioning Relay Therapeutics as a potential first mover in this space, and opening the door to another potential blockbuster.

All of these factors represent critical components that need to be taken into account when valuing the company.

The Standalone Path

Given the significant progress across these diverse therapeutic areas, we need to start seriously considering the scenario where Relay Therapeutics remains a standalone entity.

As their pipeline increases in value every day, the potential acquisition price climbs right along with it. The company is becoming more expensive and, consequently, less accessible for potential suitors. That’s not a bad thing at all.

While large pharmaceutical players like AstraZeneca or Pfizer may very well be interested, Relay is currently in a position where it can afford to reject undervalued acquisition offers and continue executing on its own.

A key factor here is the company’s strong financial position. As of early 2026, Relay held approximately $555 million in cash and investments, with management guiding runway into 2029.

That’s a very comfortable cushion.

Unlike many biotech companies, Relay is not forced to seek a buyer just to fund expensive clinical trials. It has the flexibility to advance Zovegalisib all the way through potential approval on its own.

It’s also important not to overlook the Dynamo platform, which represents far more than just a tool for developing a single drug. I go into more detail on this in my original article, it was actually one of the key reasons why I found the company so compelling and decided to invest.

The combination of artificial intelligence, machine learning, and advanced structural biology enables the targeting of previously undruggable biological mechanisms.

Selling the company at this stage would effectively mean giving up the broader upside of this innovation platform, whose value could compound significantly over time as more drugs are successfully developed and validated.

Diversification

As already mentioned, Relay Therapeutics is also gradually diversifying its portfolio. Beyond oncology indications, it is expanding into new areas where competition remains limited, while also generating revenue through additional programs such as lirafugratinib (RLY-4008).

That’s the reality.

As development progresses and the stock price continues to perform, the overall value of the company keeps increasing. Any potential acquisition at this stage would already require a significant premium.

I would argue that if no acquisition materializes in 2026, the probability of Relay choosing to remain independent increases meaningfully, at least until key clinical milestones are achieved.

Summary

Relay Therapeutics is reinforcing its position as a category leader in 2026, with zovegalisib (RLY-2608) redefining the treatment landscape for HR+/HER2− breast cancer. The FDA’s Breakthrough Therapy Designation, along with the involvement of top-tier experts like Hope S. Rugo, further validates the exceptional potential of this molecule, whose key advantage lies in its clean safety profile.

While competitors continue to struggle with liver toxicity, Relay has a clear path toward effective triple-combination regimens, the key to capturing this market.

The recent multi-billion-dollar acquisition by Novartis may have removed one potential buyer, but it simultaneously validated the massive value of selective PI3Kα inhibitors, positioning AstraZeneca as the leading candidate for a potential acquisition, next to Pfizer.

Thanks to its strong cash runway through 2029 and the unique Dynamo platform, Relay is under no pressure to sell and can continue compounding value independently.

The next major milestone is May 20, 2026, at the ISSVA Congress, where the company is expected to present clinical data from the first 20 patients with vascular anomalies.

Success in this indication would open up an entirely new multi-billion-dollar market with no direct competition, and would firmly demonstrate that Relay’s technological potential extends well beyond traditional oncology.

Thanks so much for reading, and see you next time!

9.4.2026 ~ The Value Philosopher

If you enjoyed this article and want to read more about the intersection of macroeconomics, technology, and investing, consider subscribing.

I believe the market recently reacted to the ISSVA conference announcement. Typically, when there's a "late-breaking presentation" the data should be surprisingly good.

I asked Gemini some context about it:

"Conferences reserve late-breaking slots for data that is highly significant, paradigm-shifting, or exceptionally positive. They do not give these coveted spots to failed trials or mediocre, inconclusive data. When institutional funds saw the phrase "Late Breaking" attached to an upcoming 20-patient efficacy readout, they instantly translated it to: The data is going to be incredibly good."